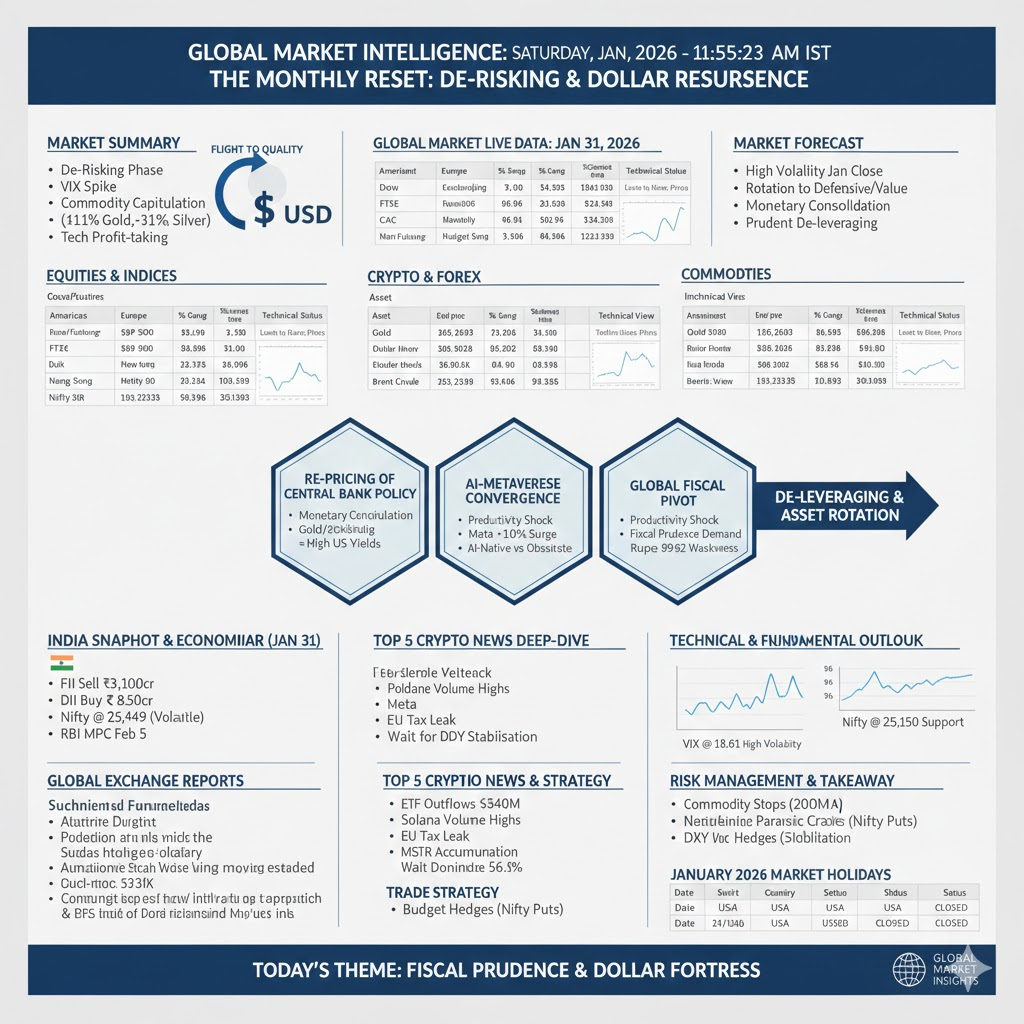

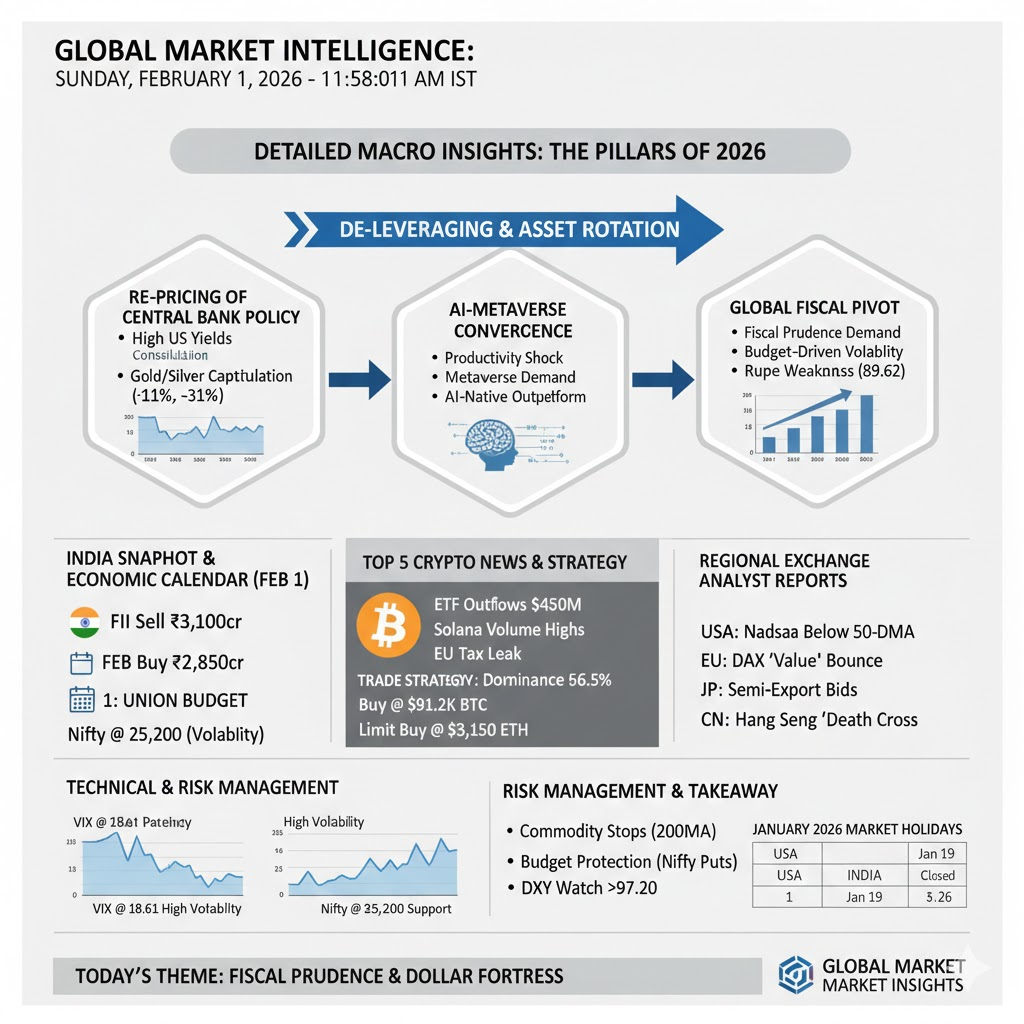

As January 2026 comes to a close, global markets are grappling with a complex transition phase marked by a sharp resurgence in the U.S. Dollar Index (96.86) and a significant “risk-off” move in technology and precious metals. The primary narrative for today, January 31, is the massive capitulation in Gold (-11.39%) and Silver (-31.37%), as institutional investors liquidate winning commodity positions to cover margins and pivot back into the Greenback. While U.S. futures show a defensive “sell-side” bias, European and some Asian pockets are staging a late-month value recovery, particularly in the banking and industrial sectors.

Market Reaction: We anticipate a high-volatility close for the month. The market is effectively pricing in a “Monetary Consolidation” after the parabolic run-up in metals. For the coming week, we expect a rotation away from overextended growth stocks into Dividend Yield and Defensive Healthcare. For the Indian market, the focus is entirely on the Union Budget (Feb 1), with the Nifty likely to see extreme intraday whipsaws as traders position themselves for fiscal announcements. The broad global sentiment today is one of “Prudent De-leveraging.”

| Continent | Index / Exchange | Live/Futures Price | % Change | Technical Status | Fundamental Driver |

| Americas | Dow Jones (USA) | 48,892.47 | -0.36% | Testing 50-DMA | Industrial Fatigue |

| S&P 500 (USA) | 6,939.03 | -0.43% | Below 20-SMA | Tech Profit Take | |

| Nasdaq 100 (USA) | 25,670.00 | -1.27% | Bearish Engulfing | Yield Spike | |

| Europe | FTSE 100 (UK) | 10,189.50 | +0.34% | Testing Pivot | Mining Recovery |

| DAX 40 (Germany) | 24,616.00 | +0.91% | Recovery Bounce | Value Buying | |

| CAC 40 (France) | 8,136.50 | +0.67% | Support Held | Luxury Resilience | |

| Asia-Pacific | Nikkei 225 (Japan) | 53,477.50 | +0.32% | Mean Reversion | Semi-Export Bids |

| Hang Seng (HK) | 27,329.50 | -1.83% | Bearish Trend | China Tech Slump | |

| Nifty 50 (India) | 25,449.70 | +0.13% | Budget Holding | Institutional Bids |

| Asset Class | Instrument | Live Price | % Change | Technical View |

| Crypto | Bitcoin (BTC) | $93,120.00 | -0.75% | Support at $92.5k |

| Ethereum (ETH) | $3,180.40 | -1.10% | Below $3.2k Floor | |

| Forex | Dollar Index | 96.86 | +0.75% | Bullish Breakout |

| USD/INR | 89.62 | +0.35% | Rupee Weakness | |

| Commodities | Gold Futures | $4,763.10 | -11.39% | Parabolic Crash |

| Silver Futures | $78.83 | -31.37% | Liquidation Mania | |

| Brent Crude | $70.69 | -0.03% | Sideways |

Institutional Activity (Jan 31 – Closing Summary):

Economic Calendar (India Focus):

How to Trade Crypto Today:

The strategy for January 31 is “Defensive Patience.” The surge in the Dollar Index (DXY) is creating a headwind for all risk assets. For Bitcoin, avoid buying the $93k bounce; instead, wait for a potential sweep of the $91,200 support level. For Ethereum, the $3,150 level is a high-probability “Limit Buy” zone. Tip: In high-volatility closes, “Cash is a Position.” Wait for the February 1 reset before going long on Altcoins.

The narrative of early 2026 is the “Re-Pricing of Central Bank Policy.” The massive capitulation in Gold (-11%) and Silver (-31%) seen today is not just a price correction; it is a signal that the “Mania Phase” of commodity hedging has hit a wall. Capital is now returning to the U.S. Dollar as a “Fortress Asset,” driven by the realization that U.S. yields will likely remain “Higher for Longer” to combat structural service-sector inflation.

The “AI-Metaverse Convergence” is the second pillar. While traditional industrials are struggling, Meta (META) and NVIDIA are seeing unprecedented demand for “Spatial AI” hardware. This “Productivity Shock” is allowing Big Tech to maintain margins even as labor and energy costs rise. We are witnessing a two-tier stock market: firms that are AI-native and firms that are AI-obsolete. The latter are being aggressively sold by institutional desks.

Finally, the “Global Fiscal Pivot” is reaching a crescendo, with India’s Union Budget serving as the primary test case for Emerging Markets. Investors are no longer looking for “Growth at any cost”; they are looking for “Fiscal Prudence.” Any country that signals a widening deficit without a clear path to infrastructure-led ROI is seeing its currency punished. The Rupee’s dip to 89.62 reflects this pre-budget anxiety.

| Date | Country | Occasion | Market Status |

| Jan 1 | USA / India | New Year’s Day | CLOSED |

| Jan 19 | USA | MLK Jr. Day | CLOSED |

| Jan 26 | India | Republic Day | CLOSED |

How to View the Global Markets Today:

The market is in an “Institutional Re-Balancing” phase. The violence of the commodity sell-off suggests that leveraged positions are being forcibly unwound. Do not fight the trend; wait for the “Mean Reversion” to complete.

Risk Management Analysis:

Important Takeaway:

The theme of January 31 is “Fiscal Prudence & Dollar Fortress.” Stability is being prioritized over growth. Position yourself in assets that benefit from high yields and AI-driven productivity, and avoid the “Hope-Trade” in overextended commodities.

aiTrendview Global Disclaimer

This report is fully AI-generated and is provided strictly for informational and educational use only. It is not investment advice, financial guidance, legal opinion, tax consultation, or professional recommendation of any kind. aiTrendview and its operators are not SEBI-registered research analysts, investment advisers, or portfolio managers. All data is automatically compiled from public sources that may contain inaccuracies, delays, or missing information. If you act on this content without verifying it independently, that is entirely your responsibility. Nothing in this report is a recommendation to buy, sell, hold, or speculate in any asset or security. aiTrendview, its creators, developers, affiliates, and associated AI systems accept zero liability for financial loss, legal trouble, or personal consequences arising from the use of this material. By reading or using this report, you accept full responsibility for your decisions. Unauthorized copying, redistribution, or modification of this content is prohibited and may result in legal action under intellectual property and compliance laws.