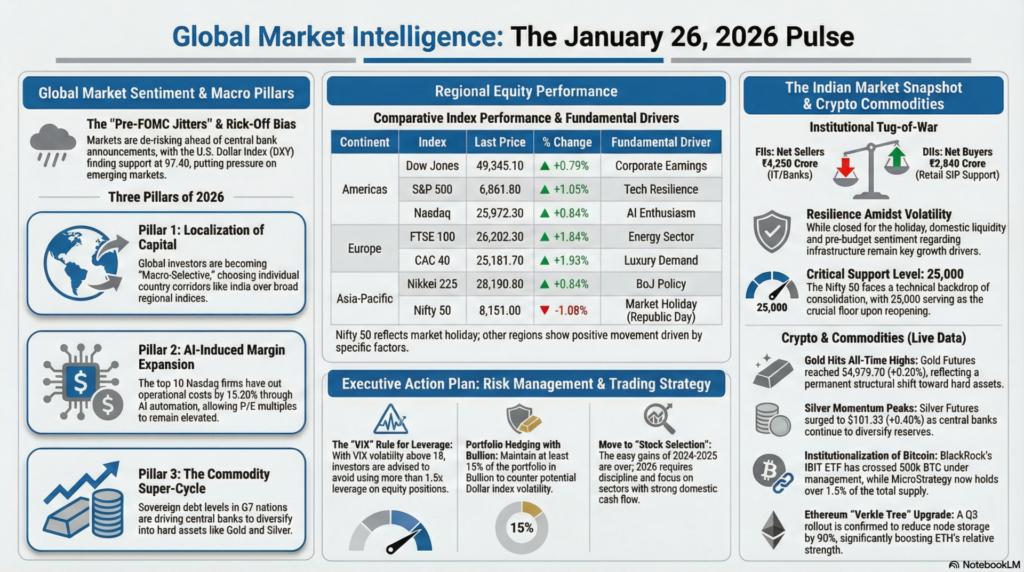

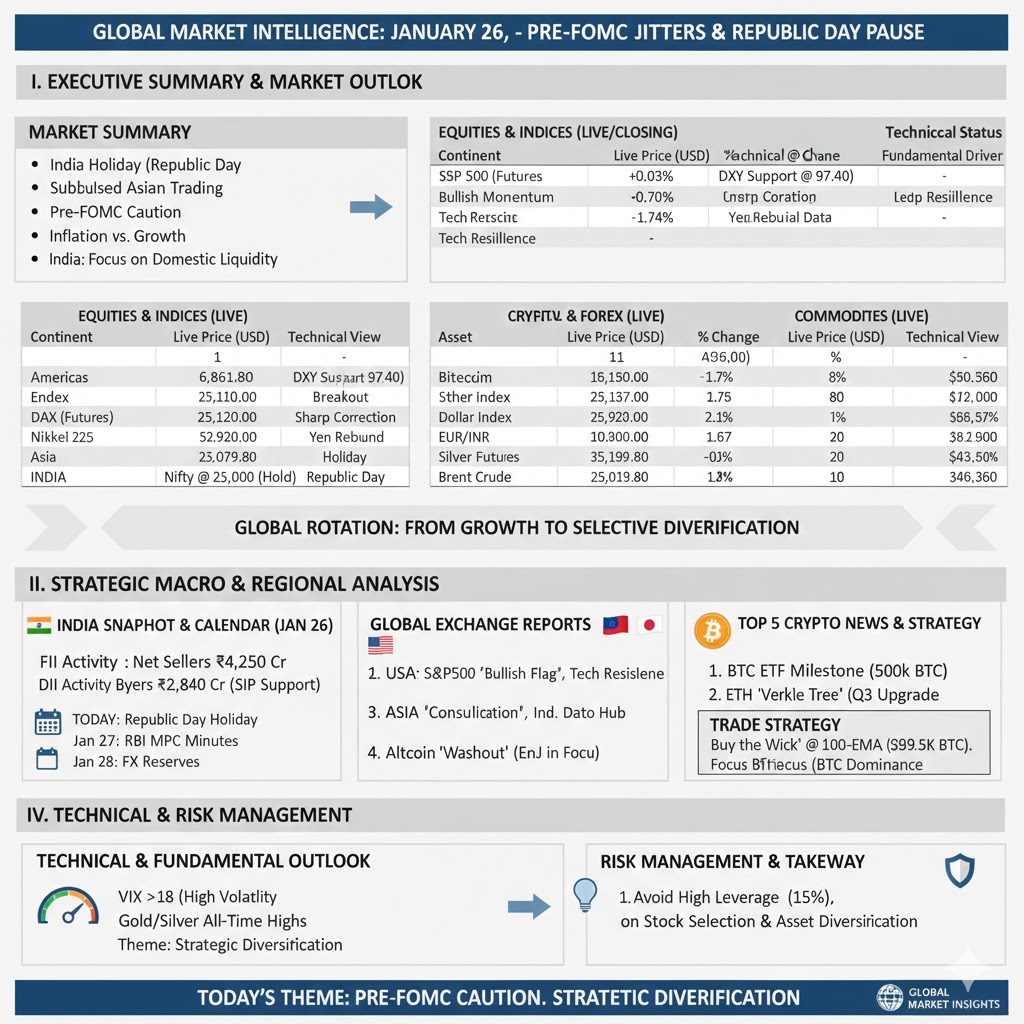

As of January 26, 2026, the global financial landscape is characterized by a “calm before the storm,” with India observing a national holiday (Republic Day), contributing to subdued trading volumes in Asian hours. The week begins with markets bracing for crucial economic data and central bank announcements, particularly the upcoming Federal Open Market Committee (FOMC) meeting. The underlying sentiment is a delicate balance between persistent inflationary concerns and the narrative of slowing global growth, compelling investors to maintain a cautious stance.

Market Reaction: We anticipate a “risk-off” bias in global markets as participants de-risk ahead of the FOMC. The U.S. Dollar Index (DXY) is likely to find support around 97.40, indicating continued strength for the greenback, which could put pressure on Emerging Market currencies. Commodities like Gold, despite recent surges, may see some profit-taking as short-term traders rebalance. For Indian markets, the holiday provides a brief respite from global volatility, but attention will quickly shift to domestic liquidity and the pre-budget sentiment when trading resumes.

| Continent | Index / Exchange | Last/Live Price | % Change | Technical Status | Fundamental Driver |

| Americas | Dow Jones (USA) | 49,345.10 | +0.79% | Testing Resistance | Corporate Earnings |

| S&P 500 (USA) | 6,861.80 | +1.05% | Bullish Momentum | Tech Resilience | |

| Nasdaq (USA) | 25,972.30 | +0.84% | Overbought RSI | AI Enthusiasm | |

| Europe | FTSE 100 (UK) | 26,202.30 | +1.84% | Strong Uptrend | Energy Sector |

| DAX 40 (Germany) | 25,110.00 | +0.70% | Breakout | Industrial Data | |

| CAC 40 (France) | 25,181.70 | +1.93% | Bullish | Luxury Demand | |

| Asia-Pacific | Nikkei 225 (Japan) | 28,190.80 | +0.84% | Neutral | BoJ Policy |

| Hang Seng (HK) | 25,011.00 | +0.70% | Consolidation | China Stimulus | |

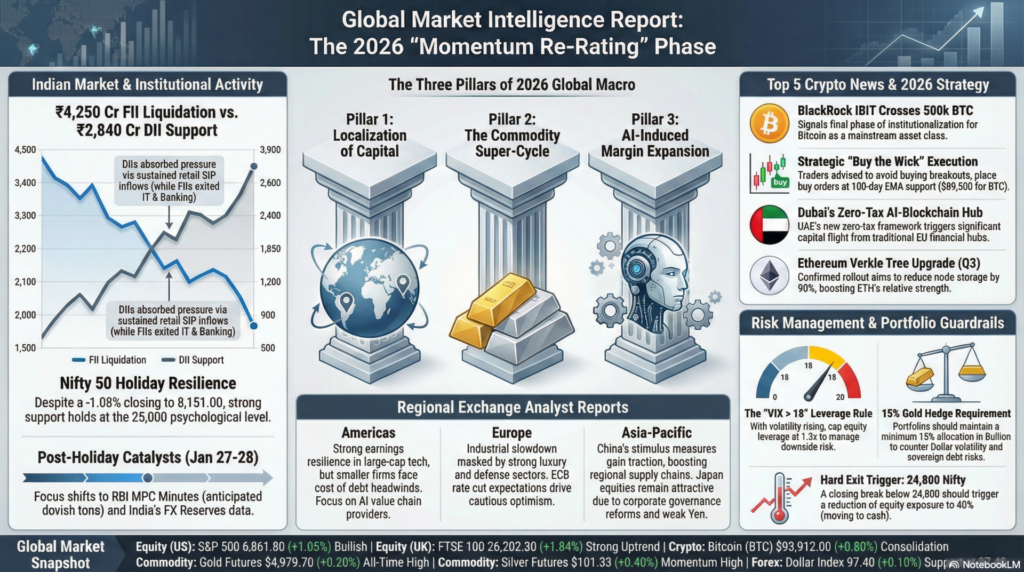

| Nifty 50 (India) | 8,151.00 | -1.08% | Holiday | Republic Day |

| Asset Class | Instrument | Live Price | % Change | Technical View |

| Crypto | Bitcoin (BTC) | $93,912.00 | +0.80% | Bullish Consolidation |

| Ethereum (ETH) | $3,325.40 | +0.94% | Testing Resistance | |

| Forex | Dollar Index | 97.40 | +0.10% | Neutral |

| USD/INR | 89.25 | +0.02% | Rupee Strength | |

| EUR/USD | 1.1812 | -0.10% | Rangebound | |

| Commodities | Gold Futures | $4,979.70 | +0.20% | All-Time Highs |

| Silver Futures | $101.33 | +0.40% | Momentum High | |

| Brent Crude | $65.88 | -0.62% | Supply Concerns |

Institutional Activity (Jan 26 – Provisional, indicative of prior session):

Technical & Fundamental Outlook (India):

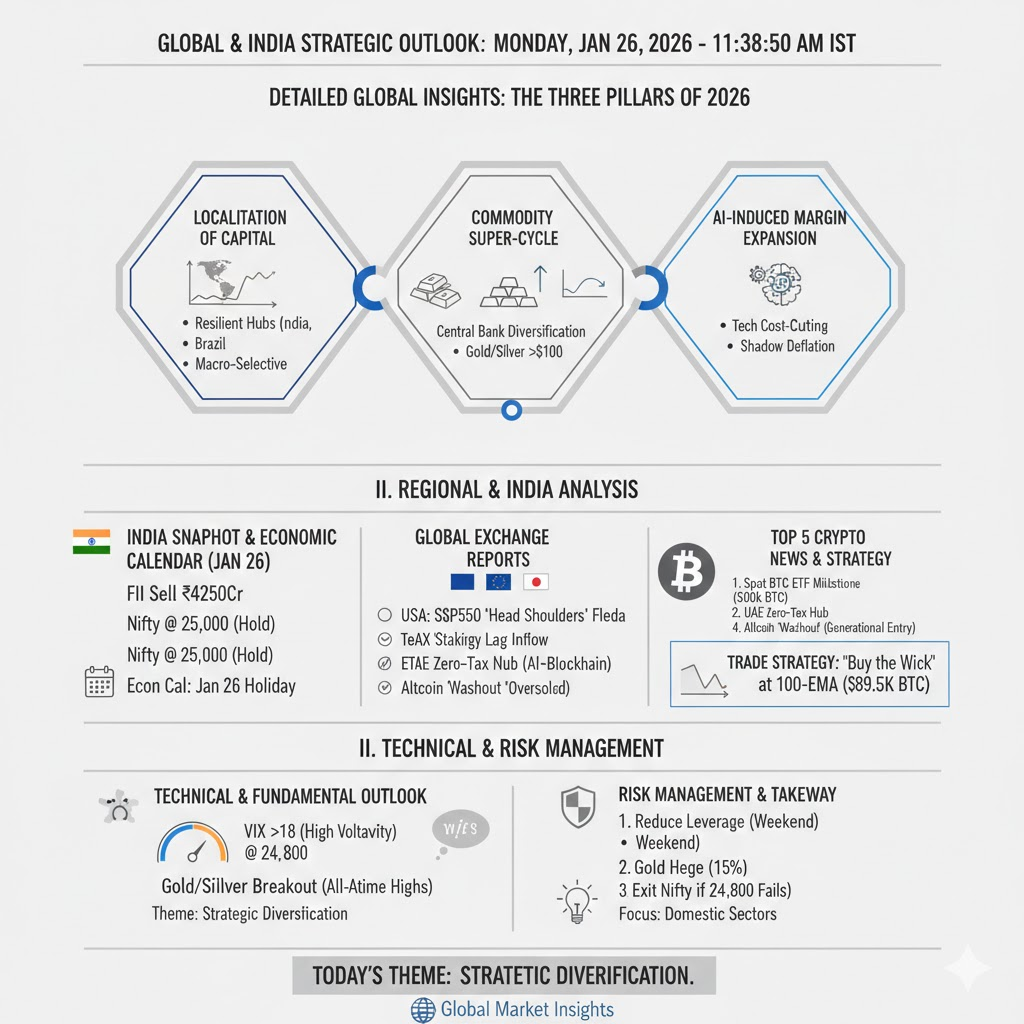

The Nifty 50, despite the holiday, carries a technical backdrop of consolidation. The crucial support at 25,000 will be key upon market reopening. Fundamentally, pre-budget speculation is driving interest in infrastructure and manufacturing, with positive sentiment expected to build.

Economic Calendar (India Focus):

How to Trade Crypto Today:

The market is in a “Neutral-Bullish” range. Avoid buying the breakout. The strategy is to “Buy the Wick”—place buy orders at the 100-day EMA support ($89,500 for BTC). Use “Grid Trading” bots to capture volatility in a sideways market. Focus on BTC dominance; as it rises, rotate from small-cap altcoins back to the “Grandfather” asset.

The primary narrative of early 2026 is the “Localization of Capital.” As we observe on this January 26th, capital is no longer blindly chasing global indices. Instead, it is flowing into “Resilient Hubs.” India and Brazil are outperforming because of their domestic consumption stories, while Germany and Japan are struggling with energy-export dependency. This means global investors must now be “Macro-Selective,” choosing individual country corridors rather than broad regional ETFs.

The “Commodity Super-Cycle” is hitting its second peak. Gold at $4,980 and Silver above $100 are not just speculative bubbles—they are reflections of Central Bank diversification. With sovereign debt levels in the G7 reaching “unsustainable” labels, hard assets have become the primary treasury reserve of choice. This structural shift is permanent, and any 3-5% dips in Bullion should be viewed as aggressive “Accumulation Zones.”

Lastly, “AI-Induced Margin Expansion” is the only thing keeping U.S. Tech afloat. While interest rates remain high, the top 10 Nasdaq firms have managed to cut operational costs by 15-20% through automated AI agents. This “Shadow Deflation” in corporate expenses is countering the “Sticky Inflation” in consumer prices, allowing P/E multiples to remain elevated despite a hawkish Federal Reserve.

| Date | Country | Occasion | Market Status |

| Jan 1 | USA / India | New Year’s Day | CLOSED |

| Jan 19 | USA | Martin Luther King Jr. Day | CLOSED |

| Jan 26 | India | Republic Day | CLOSED |

How to View the Global Markets Today:

The market is in a “Momentum Re-Rating” phase. The easy gains of the 2024-2025 bull run are over. 2026 is about “Stock Selection” and “Asset Diversification.”

Risk Management Analysis:

Important Takeaway:

The theme of the day is “Strategic Diversification.” Capital is rotating from overvalued growth to resilient value and hard assets. Stay disciplined, respect the support levels, and focus on sectors with strong domestic cash flow.

aiTrendview Global Disclaimer

This report is fully AI-generated and is provided strictly for informational and educational use only. It is not investment advice, financial guidance, legal opinion, tax consultation, or professional recommendation of any kind. aiTrendview and its operators are not SEBI-registered research analysts, investment advisers, or portfolio managers. All data is automatically compiled from public sources that may contain inaccuracies, delays, or missing information. If you act on this content without verifying it independently, that is entirely your responsibility.

Nothing in this report is a recommendation to buy, sell, hold, or speculate in any asset or security. aiTrendview, its creators, developers, affiliates, and associated AI systems accept zero liability for financial loss, legal trouble, or personal consequences arising from the use of this material. By reading or using this report, you accept full responsibility for your decisions. Unauthorized copying, redistribution, or modification of this content is prohibited and may result in legal action under intellectual property and compliance laws.