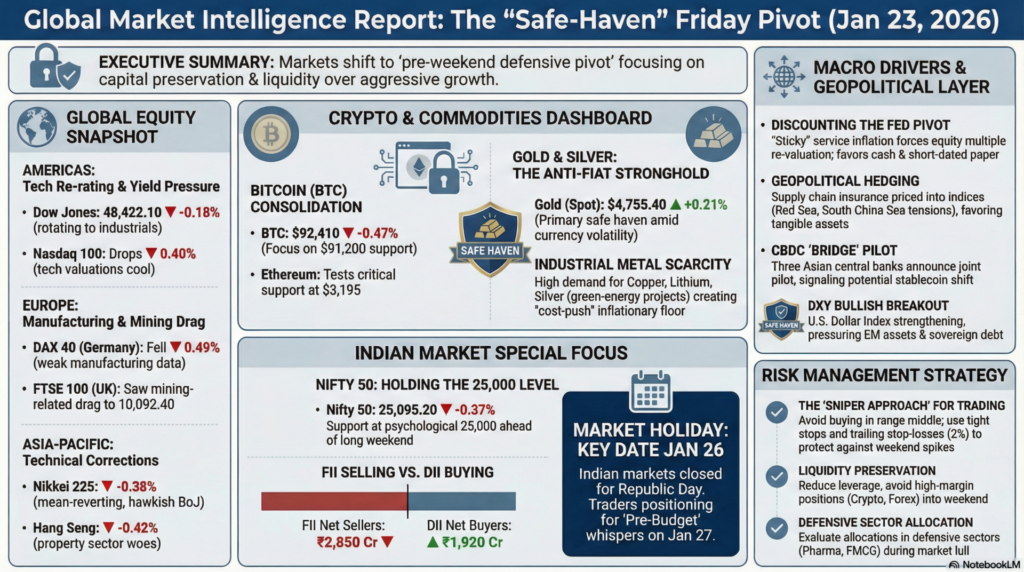

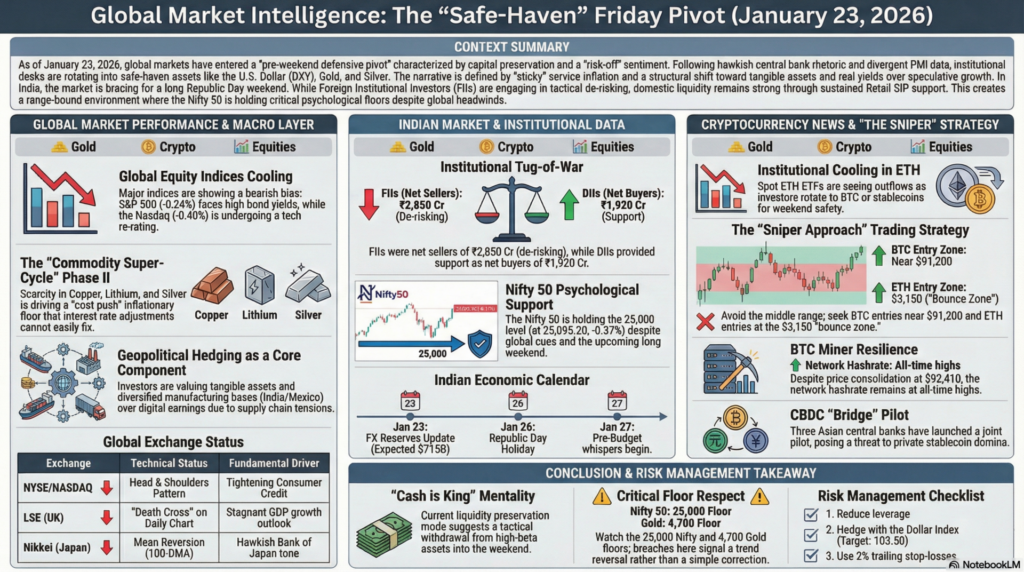

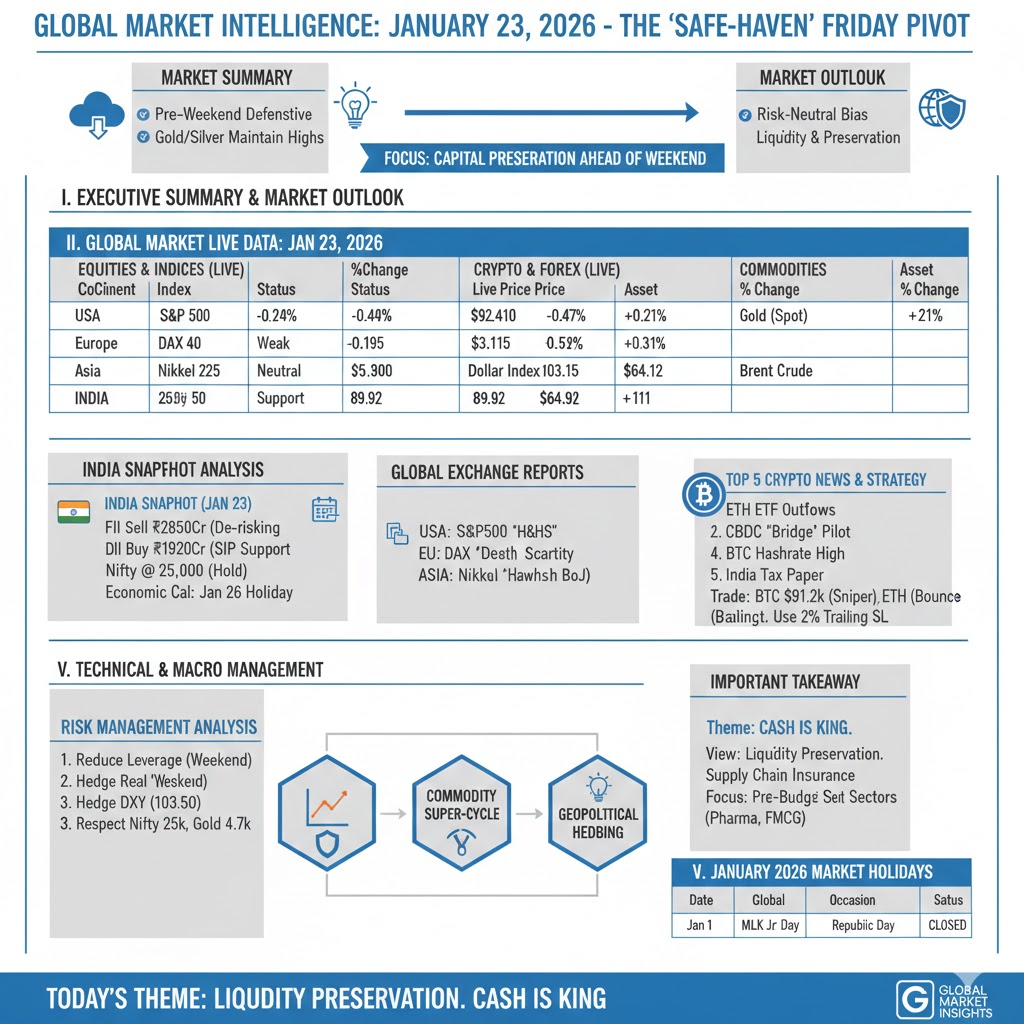

As of January 23, 2026, the global financial landscape is characterized by a “pre-weekend defensive pivot.” Following a week of divergent PMI data and hawkish central bank rhetoric, markets are entering a consolidation phase. The primary focus today is on the stabilization of the U.S. Dollar Index (DXY) near 103.00 and the persistent strength in the “anti-fiat” complex, with Gold and Silver maintaining their elevated floors. As we approach the final trading week of January, institutional desks are prioritizing liquidity and “capital preservation” over aggressive growth bets.

Market Reaction: We anticipate a “risk-neutral” sentiment with a slight bearish bias for equity indices as traders limit exposure ahead of the weekend. The strengthening Dollar is likely to keep Emerging Market (EM) assets under pressure, particularly in the currency and sovereign debt sectors. However, the “Buy the Dip” mentality remains prevalent in the energy and industrial metals space, driven by supply-side constraints. For India, expect a quiet session as domestic players prepare for the upcoming long Republic Day weekend, with low volatility but consistent DII support.

| Continent | Index / Exchange | Live Price | % Change | Technical Status | Fundamental Driver |

| Americas | Dow Jones (USA) | 48,422.10 | -0.18% | Testing 20-DMA | Industrial Rotation |

| S&P 500 (USA) | 6,795.50 | -0.24% | Bearish Crossover | High Bond Yields | |

| Nasdaq 100 (USA) | 24,880.00 | -0.40% | Overbought Cooling | Tech Re-rating | |

| Europe | FTSE 100 (UK) | 10,092.40 | -0.20% | Sideways | Mining Drag |

| DAX 40 (Germany) | 19,012.30 | -0.49% | Below 50-DMA | Weak Mfg. Data | |

| CAC 40 (France) | 7,985.60 | -0.31% | Support at 7.9k | Luxury Volatility | |

| Asia-Pacific | Nikkei 225 (Japan) | 52,210.00 | -0.38% | Neutral RSI | Yen Stabilization |

| Hang Seng (HK) | 26,105.40 | -0.42% | Bearish Channel | Property Woes | |

| Nifty 50 (India) | 25,095.20 | -0.37% | Flag Support | Long Weekend Prep |

| Asset Class | Instrument | Live Price | % Change | Technical View |

| Crypto | Bitcoin (BTC) | $92,410.00 | -0.47% | Consolidation |

| Ethereum (ETH) | $3,195.80 | -0.52% | Critical Support | |

| Forex | Dollar Index | 103.15 | +0.29% | Bullish Breakout |

| USD/INR | 89.92 | +0.11% | Rupee Weakness | |

| EUR/USD | 1.1585 | -0.30% | Testing 1.15 Support | |

| Commodities | Gold (Spot) | $4,755.40 | +0.21% | Safe Haven High |

| Silver (Spot) | $95.40 | +0.31% | Momentum Hold | |

| Brent Crude | $64.12 | +0.42% | Supply Concerns |

FII & DII Activity (Jan 23 – Provisional):

Economic Calendar (India):

How to Trade Crypto Today:

In a “Risk-Off” environment, the best strategy is “The Sniper Approach.” Avoid buying the middle of the range. For BTC, look for entries near the $91,200 support with a tight stop-loss. For Ethereum, the $3,150 level is a high-probability “bounce zone.” Trading Tip: Use “Trailing Stop Losses” of 2% to protect against weekend liquidity spikes. Focus on BTC dominance; as it rises, avoid “shitcoins” and stick to large-cap liquidity.

The primary narrative of late January 2026 is the “Discounting of the Fed Pivot.” While markets spent late 2025 hoping for rapid rate cuts, the reality of “sticky” service inflation is forcing a re-valuation of equity multiples. This is particularly evident in the Nasdaq’s struggle to maintain its 25,000 handle. We are seeing a structural shift where “Real Yields” are the primary arbiter of asset prices, favoring cash and short-dated paper over speculative long-dated growth.

The “Commodity Super-Cycle” is entering its secondary phase. It is no longer just about energy prices; it is about “Industrial Metal Scarcity.” As global green-energy projects reach their installation peaks in 2026, the demand for Copper, Lithium, and Silver is outstripping mining capacity. This creates a “Cost-Push” inflationary floor that central banks cannot easily lower by just adjusting interest rates, leading to the current high floor in Gold prices.

Lastly, “Geopolitical Hedging” is now a permanent portfolio component. With multi-polar tensions influencing trade routes in the Red Sea and South China Sea, “Supply Chain Insurance” is being priced into indices. This is why we see the Dow Jones Industrials outperforming Tech—investors are valuing tangible assets and diversified manufacturing bases (like those in India and Mexico) over purely digital earnings.

How to View the Global Markets Today:

The market is in a “Liquidity Preservation” mode. The enthusiasm of early January has been replaced by a sober assessment of inflation and growth.

Important Takeaway:

The weekend theme is “Cash is King.” We are seeing a tactical withdrawal from high-beta assets. For Indian investors, the long weekend provides a good opportunity to evaluate “Pre-Budget” allocations in defensive sectors like Pharma and FMCG.

Risk Management Analysis:

aiTrendview Global Disclaimer This aiTrendview report is an AI-generated document provided exclusively for educational and training purposes and shall not be construed as investment, financial, legal, or tax advice in any jurisdiction.

aiTrendview and its affiliates are not SEBI-registered research analysts, investment advisers, or portfolio managers, and all information herein is automatically compiled from publicly available sources that may contain errors, delays, or omissions.

Users must independently verify all data before making any financial, commercial, or legal decisions, as no market values, performance figures, or trends contained in this report constitute guarantees or forward-looking statements.

Nothing in this publication should be interpreted as a solicitation, recommendation, or endorsement to buy, sell, or hold any security.

aiTrendview, its creators, and all associated AI systems disclaim all liability for losses or consequences arising from the use or reliance upon this content, and users accept full personal responsibility for all actions taken based on it.

Unauthorized reproduction, distribution, or modification of this AI-generated material is strictly prohibited under international copyright, compliance, and intellectual-property laws.